Capital benefit vs. pension withdrawal

It is one of the most important decisions before retirement: pension or lump-sum withdrawal? You should think carefully about which option you choose, as you will not be able to switch afterwards. Because of its lasting effects, you should make this decision well informed, in good time and with competent support, so that you can embark on your new phase of life with peace of mind.

In brief - important information on lump-sum withdrawals

Investing according to your own ideas

Amortization of the mortgage

Enabling the inheritance of pension fund assets (free beneficiaries)

Potential for tax savings

Blocking period for single premiums 3 years before retirement

Possible application period of up to 3 years

In brief - Important information on drawing a pension

Guarantees an eternally high income: Regularity

Protection against old-age risk: Lifelong payout

Hedging against investment risk: independent of stock market volatility

Protection of the life partner in the event of death: spouse's pension

Elimination of asset management expenses for investments

Less tax & more flexibility thanks to lump-sum benefits

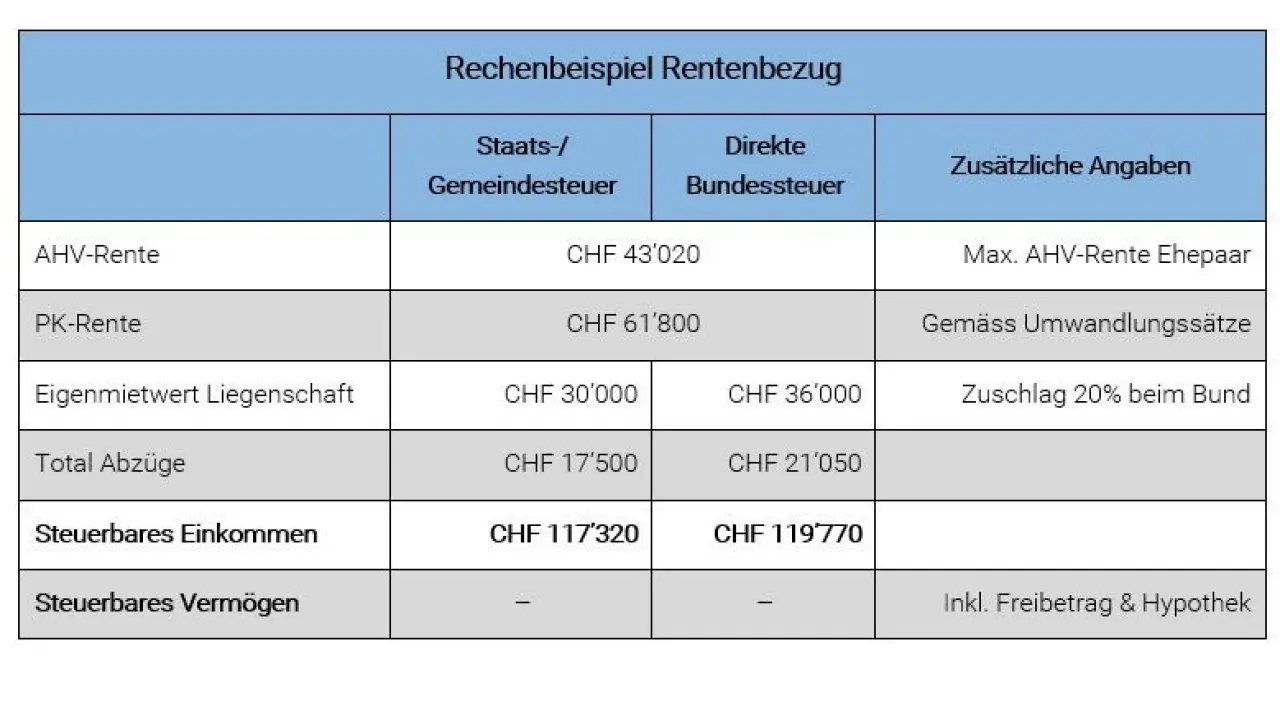

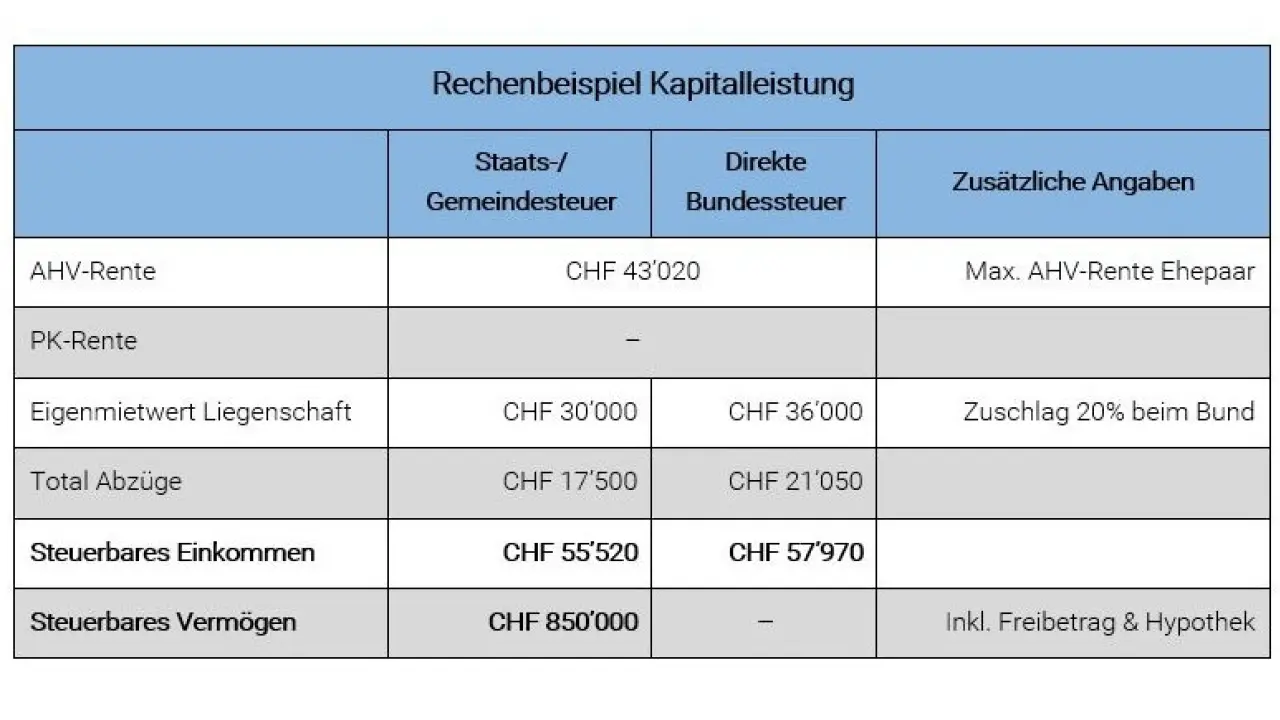

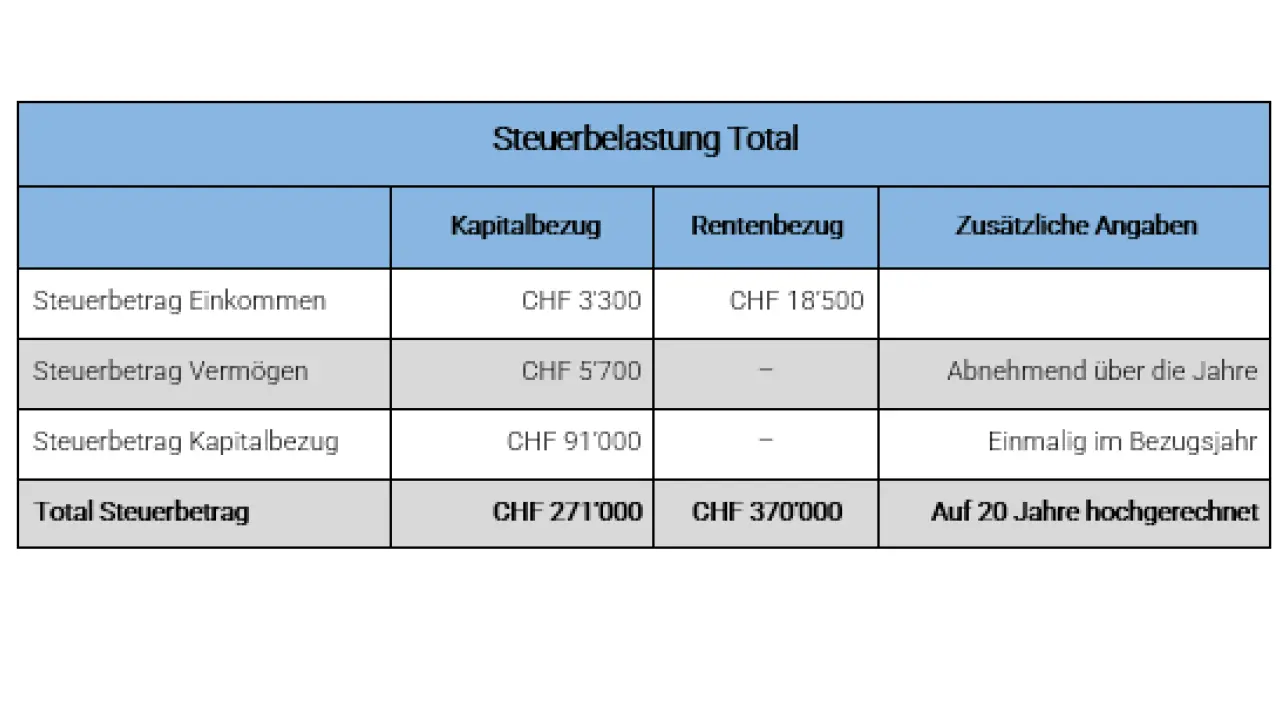

Saving taxes is also possible after retirement. The logic behind this is simple: achieve as low an income as possible. The higher the taxable income, the higher the tax rate and the associated tax liability. So if taxable income is reduced by the pension fund pension, less tax is due each year. The lump-sum withdrawal is also taxed, but at a pension rate that is lower than the ordinary tax rate: one fifth of the ordinary rate for direct federal tax and a maximum of 4.5% of the rate-determining assets (lump-sum withdrawal per person in a calendar year) for cantonal tax in the canton of Basel-Landschaft. The effect of the lump-sum payment is illustrated in the following calculation example.

Tax comparison between lump-sum withdrawal and pension

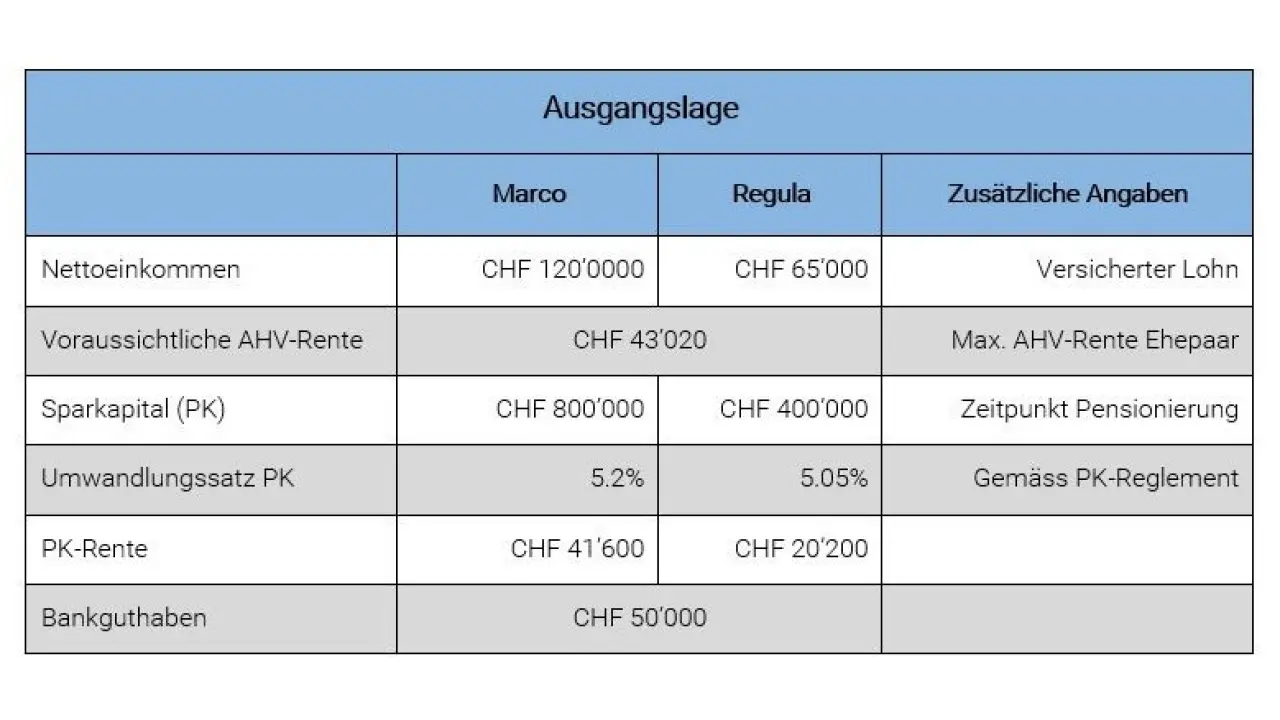

Marco and Regula Sprenger are married and live together in a detached house in Muttenz. They are both looking forward to retiring in a few years and starting a new chapter in their lives. The only thing that unsettles them is whether they should withdraw their 2nd pillar savings capital as a lump sum or a pension. They therefore turn to their trustee for advice on lump-sum payments and pension withdrawals. The following key data is given:

Both Marco and Regula are healthy. We therefore assume that they will reach the statistical life expectancy (she 87, he 85 years).

The property has a tax value of CHF 350,000

The apartment is encumbered with a mortgage of CHF 600,000

Note: For reasons of simplification, various factors are not included in this example (e.g. asset and administration costs as well as investment income or capital consumption when withdrawing capital).